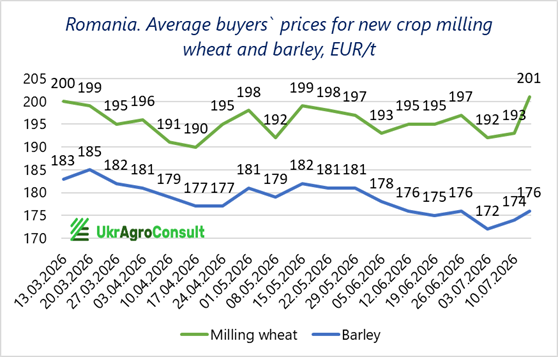

Romanian milling wheat prices jump reacting to shipping restrictions in the Azov region

14 July, 2026 at 15:07

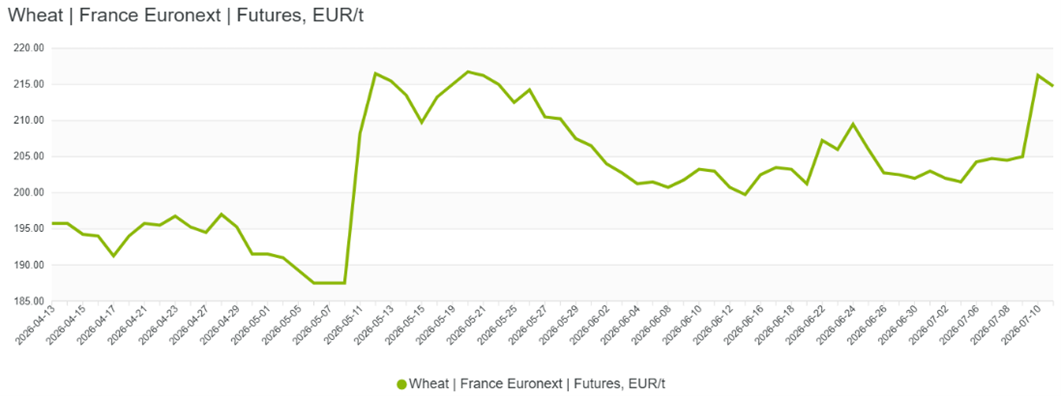

The latest shipping restrictions in the Sea of Azov and Kerch Straight significantly influenced European prices, making Matif wheat jump by EUR 10/mt on Friday.

And while European market is now evaluating further risks of lower supplies from russia, local prices in major exporters, including Romania, began the week with significant reaction.

Thus, currently the average purchasing price of Romanian milling wheat (12%) reached to EUR 201/mt CPT, or up EUR 8/mt compared to Friday level.

The price of 12.5% milling wheat rose to EUR 205/mt CPT (+EUR 7/mt). Buyers are looking towards Constanta as a safer, guaranteed alternative for prompt Black Sea grain supplies.

Market is watching how the situation unfolds, particularly in July, when traders should execute contracts for large volumes of wheat, sold at international tenders. If the blockage persists, this should further attract attention to a safer routes and support the prices for Romanian, Bulgarian as well French wheat.

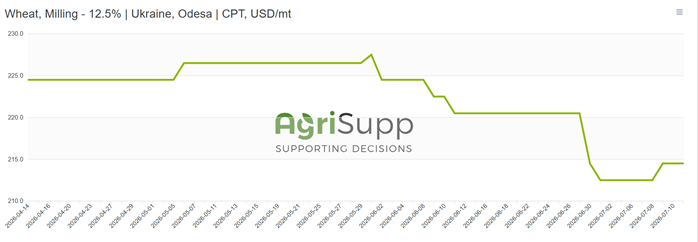

In Ukraine, there is also a growing sense that prices have already bottomed out and have gained a couple of dollars over the past week. This is happening despite high initial yields and very promising crop conditions. Some market participants have raised their production estimates to more than 24 million tonnes, compared with 23.3 million tonnes last year and the 22 million tonnes forecast issued in May.

Among domestic factors, the market is being supported by the risk of slower harvesting due to rainfall in the central regions of the country, as well as farmers’ reluctance to sell at seasonally low prices while production costs have increased.

As a result, the market has several factors supporting an upward trend. However, looking ahead, it is important not to overlook wartime logistical risks, including potential damage to port and railway infrastructure, which could disrupt export flows and put downward pressure on domestic prices.